Blog

Debunking Five M&A Myths

During our 2021 Mid-year Market Update, in addition to up-to-date transaction data and trends, our experts, M&A Director James Fisher, JD and CEO Brad Bueermann, explored some myths and misconceptions about the current M&A marketplace.

The problem with misinformation is that as a buyer you may find yourself discouraged from exploring acquisitions or mergers as a growth strategy or from inquiring on businesses that could be a great fit and expand your reach. As a seller, misinformation can lead you to compromising your fit criteria or from exploring a wider pool of buyers.

The following are the top five misconceptions we hear from advisors and from other market participants.

MYTH: Reported transaction data shows a complete view of the industry M&A marketplace.

No current reporting of annual M&A transactions–including ours–encompasses activity across the entire industry. Even if data is being reported based on publicly advertised transactions, many are private and not publicized as larger M&A deals tend to be. Details and terms are often kept confidential regardless, and, as the old adage goes, "the devil is in the details." So, comparing the data and transaction activity across firms participating in M&A can be tricky.

The community of industry thought leaders can tell you what we’re seeing amongst deals we facilitate and we can only accurately compare historical data to our own individual databases. Additionally, we can only tell you our best estimate of larger trends based on our data and expertise. This is why it’s important to understand where your information is coming from and ask: What is the source of the data? What data is being compared to produce reported trends? How large is the database? How comprehensive is the data being collected year-over-year? How are the deals facilitated?

Here at FP Transitions, our reported financial practice data and transaction trends are based on private and open market transitions facilitated by our industry-focused M&A team through a non-advocacy approach. Additionally, our valuation database tracks over 50 data point from 6,500+ financial services businesses and is managed by a team of accredited business valuation professionals.

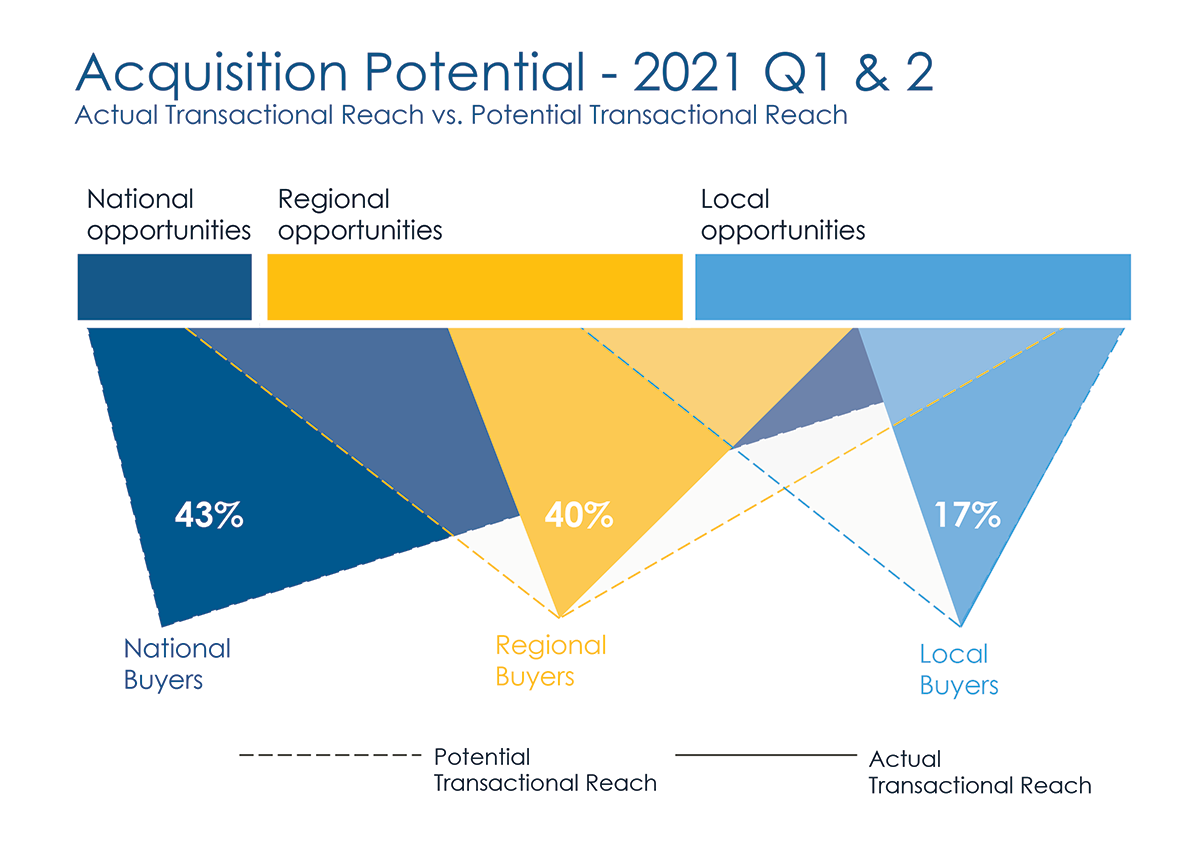

MYTH: There are really only 85 viable buyers in the marketplace.

This one is a bit of a hot button issue for us at FP Transitions. Saying that there were only 85 buyers in the marketplace does not account for the number of potential buyers in the market. Additionally, the reported number only accounts for buyers within a single M&A ecosystem, which is only a slice of the global view as we mentioned above.

While of course, in the end there can only be one buyer for every seller. In the process of choosing that buyer, each seller–at least on the FPT open market–often receives between 100-150 inquiries and has serious conversations with 5, maybe even 10, of those inquirers. There has be one “winner,” but that doesn’t make the other finalists any less viable as buyers, it just means they weren’t the exact right buyer for that particular practice.

The biggest problem with the assertion that there are only 85 buyers in the marketplace is that these buyers are almost all large aggregators. These large RIAs have great value to many advisors and investors, but, as in all things, one size does not fit all. We work with a lot of sellers who prioritize qualities like local presence, flexibility in service style, personalized financial plans, and more independent operations that can sometimes only be matched by smaller, or medium-sized, firms.

The assumption that a buyer’s viability is connected to a higher business value (over 1B AUM) or extensive acquisition experience is dangerous. It can lead to an over consolidation of the industry and homogenize the profession which is a disservice to investors.

MYTH: Many businesses are selling for more than 9x EBITDA.

From our transactions over the last 5-10 years, and from what we’ve seen reported regarding the industry marketplace, sellers should NOT expect to receive cash at closing equaling over 9x EBIDTA.

To start, the EBITDA multiples are often linked to the size of the business. The higher the value the higher multiple. This is due to things like sophistication in cash flow, operational efficiencies, and ownership structure which go hand in hand with higher business values and also make for a more desirable acquisition target.

The other factor here is that larger businesses–those that appear to be receiving 9x EBITDA and above–are typically not receiving that in cash. As with many larger acquisitions, the deal terms are more nuanced and leverage other considerations such as stock options, earn out agreements, employment contracts, or a number of other term customizations.

If you’re thinking of selling your business, it’s important to understand what your value is and why, to be realistic about what you can expect from a transaction, and to explore your options for crafting a transition that align with your priorities. The best way to do this is to perform a professional valuation which compares data from similar practices and normalizes that data for the desired terms of your transition.

MYTH: Cash is king.

In today's M&A landscape, the ability to pay full asking price–or above–in cash is not as attractive an offer as you might believe. Getting the highest amount of cash is rarely the singular priority for the sellers we work with her at FPT. Most of the sellers prioritize buyers that align with their investment philosophies, service practices, and will provide a fair deal for the practice principals as well growth opportunities to remaining staff members. They are looking for someone who will take care of their clients with little disruption to service experience.

The nature of an open-market search allows sellers to cast a wider net to find the right match. In 2020, businesses sold on the FPT Open Market, received a 15.75% higher price than the self-sourced transactions papered by FP Transitions. Additionally, sellers that leveraged an FPT Open-Market search received, on average, 11.62% higher than the most probably selling price stated in their valuation report.

As a buyer, understanding what’s most important to each individual seller and what your firm can offer to enhance the existing business is critical. Demonstrating alignment with the key stakeholder groups in the selling business–owners, team, and clients–will, for most sellers, clinch the deal.

MYTH: Business value equals selling price.

While an accurate valuation performed for the purpose of a sale can produce a number that is close to what a business ultimately sells for, it is just a starting point. There are many variables, priorities, and deal terms to be considered in price negotiation.

First of all, 100% cash transactions in an industry based on intangible, service-based assets are risky for the buyer. As such, most acquisitions include a combination of down payment and some sort of promissory note in order to mitigate risk weighted heavily toward one party. The type and length of the note will affect the overall sale price. FP Transitions valuation reports account for the purpose of the assessment from square one and provide a range of potential selling prices accounting for common deal terms.

Secondly, at FP Transitions, we have more recently seen a larger number of firms that–for strategic reasons–are willing to pay more than the stated market value. Or in our case, the most probable selling price for a particular practice. But there's almost always a very specific reason that these buyers are willing to do that. This could be due to the fact that the practice is in a desirable marketplace where that buyer would like to expand, or there's significant synergies and efficiencies that a buyer will benefit from post-sale.

Ultimately, as a buyer or seller, participating in M&A–or developing any growth strategy–comes down to assessing your own unique business, educating yourself, understanding the sources of information, exploring your options, and leveraging expert guidance.