Blog

Estimating Value Based on Recurring Revenue

Recurring revenue is one of the most important single determinants of value. Revenue produced through management fees, trails, or renewals is ongoing and reasonably predictable. Transactional revenue is more elusive and difficult to predict. While this isn’t cutting edge news, it is important to understand that recurring revenue is more predictable and presents less risk of future earnings when compared to transactional revenue. As such, when a portion of revenue is generated from transactional revenue, buyers will require a higher rate of return (discount) when compared to other market alternatives that provide more certainty.

Rule of Thumb?

It is important to understand the difference between an adjusted pricing multiple based on the specific characteristics of the business being valued versus a “rule of thumb.” A rule of thumb for the financial services industry is that businesses sell for two-times gross recurring revenue and one-times non-recurring revenue, or that they are worth five-times Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). Often sellers approach us asking if the offer they have received based on a rule of thumb is sufficient or fair. This question cannot reasonably be answered without understanding the revenue characteristics of the practice.

Rules of thumb are not based on empirical evidence and have not been examined or tested to determine their validity. A rule of thumb is merely a means of estimating value based on a rough and ready practical rule, not based on science or exact measurement.

Other definitions include “[a] theoretical market-derived unit [ ] of comparison”¹ and “a mathematical formula developed from the relationship between price and certain variables based on experience, observation, hearsay or a combination of these; usually industry specific.”² A rule of thumb is therefore used as a reasonability check for other valuation methods that are not tied directly to observed market transactions. It should never be used as a stand-alone method for valuing a business.

Adjusted Pricing Multiples

An adjusted pricing multiple is the result of a professional appraiser’s many hours of market research and analysis of the subject practice as it compares to observed prices in the market. Arriving at an adjusted pricing multiple requires an understanding of how buyers in the marketplace perceive value and what those key value drivers are. For financial services practices, this key value driver is recurring revenue. It is the difference between a practice selling for 0.27 times annual gross revenue and 2.84 times annual gross revenue.

Our observed range of annual gross revenue pricing multiples ranges from a low of 0.27 to a high of 2.84 with the central tendency being 1.85. This is quite a broad spread between high and low. Without understanding the primary value driver of these businesses, simply using a rule of thumb or average pricing metric as opposed to an adjusted pricing multiple may lead to a significant error in valuing the subject practice. Valuation errors can result in the deal being skewed toward one party as opposed to creating a fair and equitable deal for both parties, or worse, a transaction that never closes or results in one party who feels taken advantage of.

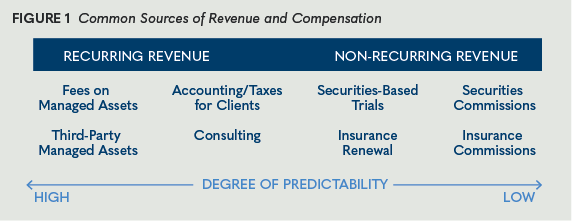

Sources of Revenue

Revenue streams, even recurring revenue streams, are seen differently depending on their degree of perceived predictability. Figure 1 shows the most common sources of compensation financial advisors receive for their services and the market’s sentiment regarding the predictability of each source of revenue.

Market demand for recurring revenue remains high and values for fee-only business types are strong. Not all fee sources are valued equally, however. Further complicating questions of value, most businesses include a combination of revenue sources with varying degrees of predictability. Determining an appropriate value for a specific business in a specific situation merits a deeper assessment than simply estimating value on a multiple of recurring revenue.

Practices in this industry are commonly categorized as fee-only, commission-based, or transactional, depending on how their advisors are compensated for their services. It’s important to remember that many people, especially those outside the advisory industry, often use the terms fee-only and commission-based interchangeably. They are indeed different and have a different impact on recurring revenue.

Fee-only advisors receive all compensation in the form of either performance-based fees or a fixed, flat, hourly percentage. These fees are typically based on the amount of assets the advisor is managing and the complexity and financial needs of the individual clients.

Commission-based advisors can receive compensation from charging fees similar to a fee-only practice, but they also receive compensation based on transactions involving a product or service. This includes insurance renewals, securities-based trails, surrender charges, and contingent deferred sales charges. Commission-based practices generally receive a mix of both recurring and non-recurring forms of compensation.

Transactional practices are those that receive compensation-based revenue on transactions involving a product or service, but the compensation is primarily non-recurring.

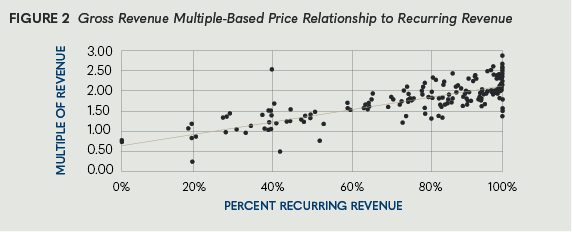

The graph in Figure 2 illustrates how recurring revenue influences the perceived value of a business by examining recent transactions (2016–2018) and the modeled relationship between the multiple that each practice sold for as compared to each practice’s reported amount of compensation that is recurring and predictable. It is important to note that the transactions used in this model were not sorted by deal terms, which can influence the final purchase price. We can see here that the market places more value on recurring, predictable forms of compensation.

Another notable observation is that there are relatively few transactions involving practices that generated less than 20% of their revenue from recurring forms of compensation. Typically, businesses that fall below this 20% threshold don’t engage in a typical asset sale as other practices do. In other words, most practices generating less than 20% recurring revenue typically transition their business and receive their value by sharing revenue with the new advisor servicing the clients if there is any future revenue generated from those clients.

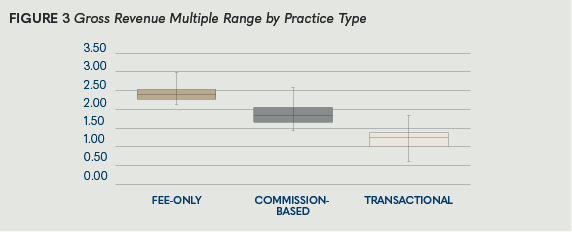

Recurring Revenue and Value

There is a clear pricing differential based on the practice type (fee-only, commission-based, or transactional) as shown in Figure 3. Fee-only practices typically sell within the range of 2.28–2.53 times gross annual revenues with the central tendency being 2.44. The median sale prices for these practices have been trending upward over the last three years.

Commission-based practices sell within a much larger range than fee-only practices. When valuing these types of practices, it is important to understand the forms of compensation the advisor receives and what restrictions there are regarding future compensation. Typically, these types of practices will sell within the multiple range of 1.66–2.05 with the central tendency being 1.85. The market for these types of practices has remained fairly level over time. In 2016, 2017, and 2018, as with fee-only practices, the median values have also trended up from the past three years, albeit at lower absolute numbers.

Lastly, transactional practices typically sell within a multiple range of 1.01–1.37 with the central tendency being 1.25. As illustrated in Figure 5.3, the central tendency for these types of businesses is toward the higher end of the range. This is a result of the transactional pricing multiples for these practices not being evenly distributed within the range of 1.01–1.37. In other words, more practices receiving transactional compensation have sold for less than a 1.25 multiple of gross revenue, but a few have sold for substantially higher. This is a result of the mixed perceptions of value for these types of practices due to their varying ability to generate future revenues.

Estimating the value of a financial services business requires reliance on the amount of recurring revenue as well as its sources and level of predictability. It is important to understand that recurring revenue presents less risk of future earnings when compared to transactional revenue and provides a relatively clearer forecast of future value.

This article is an excerpt from our 2019 Trends in Transactions and Valuation Study ©2019 FP Transitions, LLC.